💰 Making Every Rupee Count: A Simple Budget Plan That Works for Indian Families

When you’re earning ₹15,000 to ₹30,000 monthly, every single rupee matters. A simple budget plan India isn’t about complex spreadsheets or restrictive living—it’s about creating a financial system that brings peace of mind while covering essentials, building savings, and achieving family goals. Government data reveals that average monthly consumption expenditure in rural India is ₹4,247 and ₹7,078 in urban areas, showing that millions of families successfully manage on modest incomes through smart monthly budget India strategies.

📋 Table of Contents

- Why Simple Budgeting Matters for Indian Families

- The Core Budget System That Works

- ₹20,000 Salary Budget Plan

- Understanding Essential Expense Categories

- Practical Implementation Steps

- Simple Tracking Methods

- Overcoming Common Budgeting Challenges

- Building Your Emergency Safety Net

- Frequently Asked Questions

🎯 Why Simple Budgeting Matters for Indian Families

The reality of budgeting low salary India is that most families don’t fail because they spend carelessly—they struggle because they lack a clear system. Without a simple budget plan India framework, money disappears into untracked daily expenses, leaving families wondering where their salary went by month-end. Research on lower-middle-class earnings shows that rising costs in healthcare, education, and housing create mounting pressure on household finances.

A proper simple budgeting system India transforms financial chaos into clarity. It helps you avoid the common financial mistakes that keep Indian families trapped in paycheck-to-paycheck cycles. When you know exactly where money flows each month, you gain control—making conscious choices rather than reactive spending decisions.

The benefits extend beyond mere survival. Families following a structured monthly budget India plan report reduced stress, better sleep, fewer marital conflicts over money, and the ability to plan for children’s education and family goals. Even saving just ₹500 monthly creates a foundation for financial security that compounds over years.

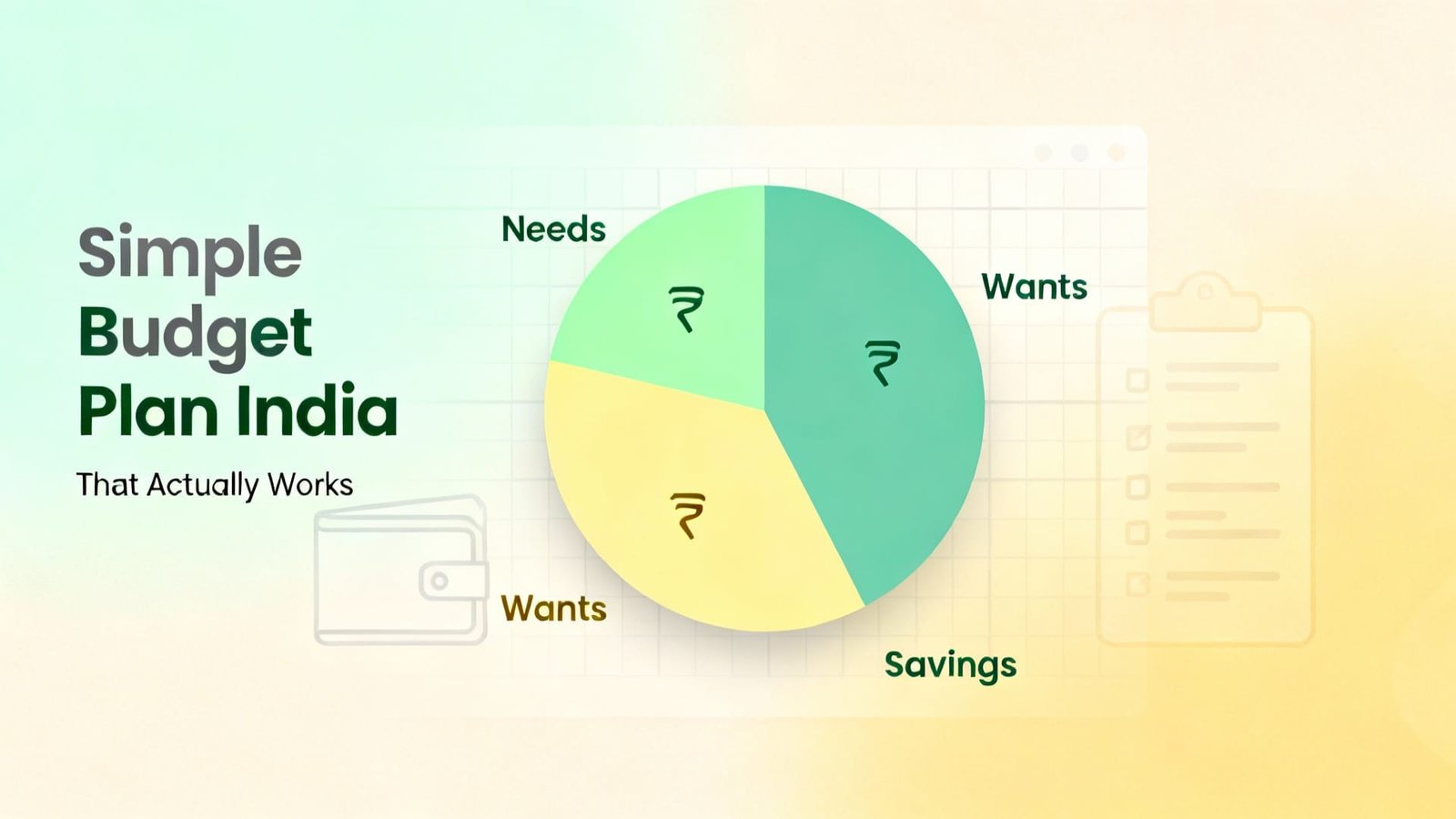

💡 The Core Budget System That Works

The most effective budget plan for low salary India is the adapted 50/30/20 rule, modified for Indian realities. While the original formula allocates 50% to needs, 30% to wants, and 20% to savings, Indian households often require adjustments based on income levels and family circumstances.

🏠 The Indian-Adapted Budget Formula

For low-income Indian families, a more realistic simple budget plan India formula looks like this:

- 60% for Essential Needs – Housing, food, utilities, transportation, healthcare, and mandatory expenses that keep the household functioning

- 25% for Lifestyle & Discretionary – Entertainment, social obligations, festivals, personal care, and quality-of-life expenses

- 15% for Savings & Debt Repayment – Emergency fund, future goals, insurance, and clearing existing debts

⚡ Reality Check: If you’re earning below ₹25,000 monthly, your essentials might consume 65-70% of income initially. That’s normal. The goal is gradual optimization through the simple budgeting system India approach, not immediate perfection.

📊 ₹20,000 Salary Budget Plan India – Practical Breakdown

Let’s examine a realistic ₹20,000 salary budget plan India for a single earner supporting themselves or a small family in a tier-2 or tier-3 city. This essential expenses plan India demonstrates how strategic allocation creates financial stability even with limited income.

| Expense Category | Monthly Amount | Percentage | Notes |

|---|---|---|---|

| 🏠 Housing (Rent/EMI) | ₹5,000 – ₹6,000 | 25-30% | Shared accommodation or smaller space in affordable areas |

| 🍚 Food & Groceries | ₹4,000 – ₹5,000 | 20-25% | Home-cooked meals, bulk buying, minimal outside food |

| ⚡ Utilities (Electricity, Water, Gas) | ₹1,200 – ₹1,500 | 6-7% | Conservative usage, energy-saving practices |

| 🚌 Transportation | ₹1,500 – ₹2,000 | 7-10% | Public transport, shared rides, bicycle for short distances |

| 📱 Mobile & Internet | ₹500 – ₹700 | 3% | Budget plans, avoid unnecessary add-ons |

| 💊 Healthcare & Medicine | ₹800 – ₹1,000 | 4-5% | Basic health insurance, preventive care, generic medicines |

| 🎬 Entertainment & Personal | ₹1,000 – ₹1,500 | 5-7% | Occasional movies, social outings, personal care |

| 💰 Savings & Emergency Fund | ₹2,000 – ₹3,000 | 10-15% | Non-negotiable automatic savings |

| 📝 Miscellaneous Buffer | ₹1,000 – ₹1,500 | 5-7% | Unexpected expenses, festivals, contingencies |

This budget plan for low salary India totals approximately ₹17,000-₹20,000, depending on individual circumstances. Financial experts suggest that even with ₹20,000 monthly income, consistent savings of ₹2,000-₹3,000 is achievable through disciplined expense management.

🔍 Understanding Essential Expense Categories

🏡 Housing Expenses (25-30% of Income)

Housing typically consumes the largest portion of any simple budget plan India. For low-income families, keeping this below 30% requires creative solutions like sharing accommodation, living in peripheral areas with good connectivity, or negotiating favorable rent terms with landlords. In rural areas or smaller towns, housing costs drop significantly, allowing more allocation to other categories.

🍽️ Food & Nutrition (20-25% of Income)

Food is non-negotiable, but smart monthly budget India planning reduces costs without compromising nutrition. Bulk purchasing of staples like rice, wheat, and lentils from wholesale markets saves 15-20%. Cooking at home instead of ordering food can cut expenses by half. Planning weekly menus prevents food waste and impulsive purchases.

🚌 Transportation (7-10% of Income)

Transportation costs vary dramatically between cities. The most effective budgeting low salary India strategy combines public transport for longer distances with walking or cycling for nearby errands. Monthly bus passes or metro cards offer significant discounts compared to daily tickets.

💊 Healthcare Planning

Healthcare represents a critical vulnerability for low-income families. Government schemes like Ayushman Bharat provide coverage up to ₹5 lakh annually for eligible families. Building a health buffer within your essential expenses plan India prevents medical emergencies from derailing your entire financial plan. Understanding where your money is safe during financial crises adds another layer of security.

⚙️ Practical Implementation Steps

Step 1: Calculate Your True Monthly Income

Start your simple budgeting system India by determining actual take-home pay after all deductions including PF, taxes, and other mandatory contributions. For irregular income earners like daily wage workers or small business owners, calculate the average of the past 3-6 months to establish a baseline.

Step 2: Track Every Expense for One Month

Before creating your budget plan for low salary India, spend one month documenting every rupee spent. This reveals hidden spending patterns—those ₹20 daily tea expenses that accumulate to ₹600 monthly, or frequent small purchases that add up significantly. Use a simple notebook or smartphone app to record transactions immediately.

Step 3: Categorize and Prioritize

Group expenses into essential needs, lifestyle wants, and savings. Identify areas where your monthly budget India can be optimized. Perhaps you’re spending ₹200 on premium mobile apps when free alternatives exist, or buying packaged snacks when homemade options cost less.

💡 Pro Tip: When implementing your simple budget plan India, start with the “save first, spend later” approach. Transfer your savings amount immediately after receiving salary, making it unavailable for spending. This reverses the common mistake of saving whatever remains at month-end (usually nothing).

Step 4: Allocate Based on Priority

Assign specific amounts to each category following the simple budgeting system India percentages. Be realistic—if rent actually costs 35% of your income, adjust other categories rather than setting unrealistic housing targets. Your essential expenses plan India must reflect actual life, not theoretical perfection.

Step 5: Create Spending Boundaries

Once allocated, treat category limits as boundaries. When the groceries budget reaches its limit, you stop buying until next month unless it’s a genuine emergency. This discipline transforms your budgeting low salary India plan from theory into practice.

📱 Simple Tracking Methods

Effective monthly budget India tracking doesn’t require expensive software or complex systems. Choose methods that match your comfort level and lifestyle.

📓 The Notebook Method

The simplest simple budget plan India tracking uses a dedicated notebook divided into categories. Write down every expense immediately under the relevant heading. At week-end, total each category to see if you’re on track. This old-school method works brilliantly for those uncomfortable with technology.

📊 The Envelope System

A powerful simple budgeting system India technique involves physical cash envelopes for each spending category. When salary arrives, withdraw cash and distribute it into labeled envelopes—groceries, transportation, entertainment, etc. Spend only what’s in each envelope. When it’s empty, spending in that category stops until next month. This creates visceral awareness of spending limits.

📲 Free Mobile Apps

For tech-comfortable users, free apps like Walnut, Money Manager, or simple Excel/Google Sheets templates automate tracking. These apps sync with bank accounts, categorize expenses automatically, and send alerts when category limits approach. Choose apps without subscription fees to maintain your budget plan for low salary India.

🏦 Bank Statement Review

Monthly bank statement analysis provides a comprehensive view of spending patterns. Most banks categorize transactions automatically. Cross-reference this with your planned essential expenses plan India to identify discrepancies and adjust accordingly.

⚠️ Overcoming Common Budgeting Challenges

Challenge 1: Irregular Income

Many Indian workers—from construction laborers to small shop owners—face irregular income streams. The simple budget plan India solution is creating a baseline budget using the lowest typical monthly earning from the past year. During higher-earning months, save the excess rather than increasing lifestyle expenses. This buffer covers lower-earning months without stress.

Challenge 2: Unexpected Expenses

Medical emergencies, vehicle repairs, or family obligations appear suddenly, derailing even the best monthly budget India plan. Build a miscellaneous buffer of 5-7% specifically for such situations. Additionally, focus on building your emergency fund systematically—even ₹100 weekly creates a ₹5,200 annual safety net.

Challenge 3: Family Pressure and Social Obligations

Indian families face significant social pressure around festivals, weddings, and family events. A realistic budgeting low salary India approach acknowledges these cultural realities. Create a separate annual allocation for major festivals and social obligations, setting aside small amounts monthly rather than scrambling during event seasons. Sometimes saying “I can contribute ₹500 instead of ₹2,000” requires courage but protects your financial stability.

Challenge 4: Lack of Financial Discipline

Starting a simple budgeting system India is easy; maintaining it requires commitment. Avoiding common financial mistakes and hidden charges like credit card fees becomes easier when you track spending religiously. Consider finding an accountability partner—a spouse, friend, or family member—who reviews your budget monthly and provides encouragement.

✅ Success Story: Rajesh, earning ₹22,000 monthly in Jaipur, struggled with constant debt until implementing a simple budget plan India. By tracking expenses and using the envelope system, he identified ₹3,000 monthly waste on unnecessary subscriptions and impulse purchases. Within 18 months, he cleared ₹40,000 debt and built a ₹25,000 emergency fund—all while supporting his family on the same income.

🛡️ Building Your Emergency Safety Net

No budget plan for low salary India is complete without an emergency fund. Financial experts recommend maintaining 3-6 months of essential expenses for emergencies. For a family spending ₹15,000 monthly on essentials, this means saving ₹45,000 to ₹90,000.

🎯 Emergency Fund Building Strategy

Building such amounts seems impossible on low income, but the simple budgeting system India approach makes it achievable through small, consistent steps:

- Start with ₹10,000 Target – Focus initially on accumulating ₹10,000, enough to handle most common emergencies like medical costs or urgent repairs

- Save Small, Save Consistently – Even ₹500 monthly becomes ₹6,000 annually. Combined with festival bonuses or extra income, reaching ₹10,000 within 12-15 months is realistic

- Park It Safely – Keep emergency funds in high-interest savings accounts or liquid mutual funds that offer both safety and easy access within 24-48 hours

- Never Touch Except True Emergencies – A new phone isn’t an emergency; medical treatment or job loss is. Maintain strict boundaries

- Rebuild After Using – If you use emergency funds, immediately restart contributions to replenish the buffer

Understanding deposit insurance and bank safety ensures your emergency fund remains secure even during financial system disruptions.

💪 Beyond Budgeting: Income Enhancement

While the essential expenses plan India optimizes spending, increasing income accelerates financial progress. Consider skill development in high-demand areas, part-time freelancing, or small side businesses that align with your abilities. Even an additional ₹2,000-₹3,000 monthly dramatically improves your financial position when properly budgeted.

Taking a 7-day money challenge can help reset financial habits and discover hidden savings opportunities within your current income.

❓ Frequently Asked Questions

A simple budget plan India on ₹15,000 requires allocating approximately ₹9,000-₹10,000 (60-65%) for essential expenses like rent, food, and utilities, ₹3,000-₹4,000 (20-25%) for discretionary spending, and ₹1,500-₹2,000 (10-15%) for savings. Share accommodation to reduce housing costs, cook at home to minimize food expenses, and use public transportation to stay within budget.

For irregular income, the best monthly budget India strategy involves calculating your lowest typical monthly earning over the past 12 months and budgeting based on that baseline. During higher-earning months, save the excess in a separate buffer account to cover lower-earning periods, ensuring consistent household expenses regardless of income fluctuations.

Start with a realistic budgeting low salary India emergency fund target of ₹10,000, which handles most common emergencies. Gradually build this to 3-6 months of essential expenses. Even saving ₹500 monthly creates ₹6,000 annually—combine this with bonuses or festival earnings to reach your emergency fund goal faster.

An essential expenses plan India includes housing (rent/EMI), food and groceries, utilities (electricity, water, gas), transportation, healthcare and medicines, mobile and internet, children’s education, and debt repayments. These typically consume 60-70% of income for low-income families, leaving 20-25% for lifestyle expenses and 10-15% for savings.

The most effective tracking for a budget plan for low salary India combines immediate expense recording (using notebook or mobile app) with weekly category reviews. The envelope system works excellently for cash transactions—allocate physical cash to different spending categories and stop spending when envelopes empty. Monthly bank statement reviews identify patterns and areas for improvement.

Yes, a simple budgeting system India makes saving possible even on ₹20,000 monthly. By allocating 60-65% to essentials, 20-25% to lifestyle, and 10-15% to savings, you can save ₹2,000-₹3,000 monthly. The key is disciplined tracking, reducing unnecessary expenses, and adopting the “save first, spend later” mindset where savings are transferred immediately upon receiving salary.

Ideally, monthly budget India planning recommends keeping housing costs below 30% of income. For low-income families, this might mean sharing accommodation, living in peripheral areas with good connectivity, or negotiating favorable rent terms. If housing exceeds 30%, compensate by reducing discretionary spending in other categories rather than cutting essential food or healthcare expenses.

Include festival expenses in your simple budget plan India by creating a dedicated annual allocation. Calculate total yearly festival spending (Diwali, Holi, family occasions) and divide by 12 months. Set aside this amount monthly in a separate account. For example, if festivals cost ₹12,000 annually, save ₹1,000 monthly so funds are available when needed without disrupting regular budgets.

🚀 Ready to Take Control of Your Finances?

Start your investment journey with India’s leading trading platforms